As we move through mid-July, the housing market remains in a state of adjustment. Higher mortgage rates have reshaped buyer demand, while many homeowners stay put, locked into lower rates. In the Bay Area, job cuts and persistent inflation add to the uncertainty, with interest rates stubbornly elevated, relatively speaking. Despite these headwinds, opportunities still exist for those who understand how to navigate this shifting landscape.

-

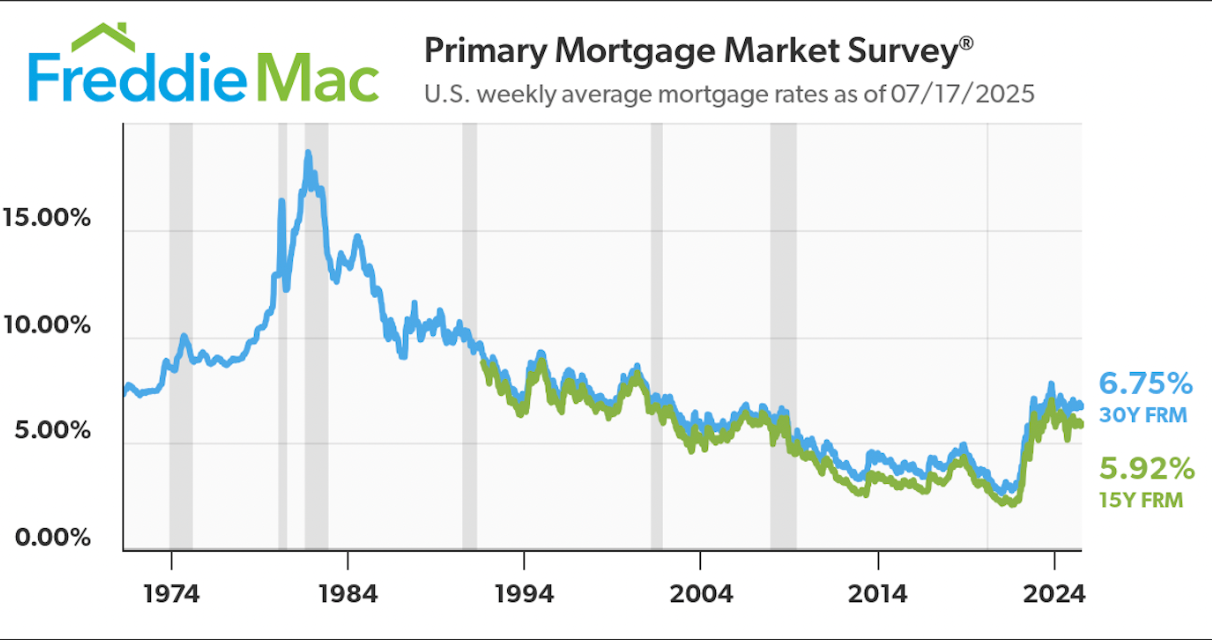

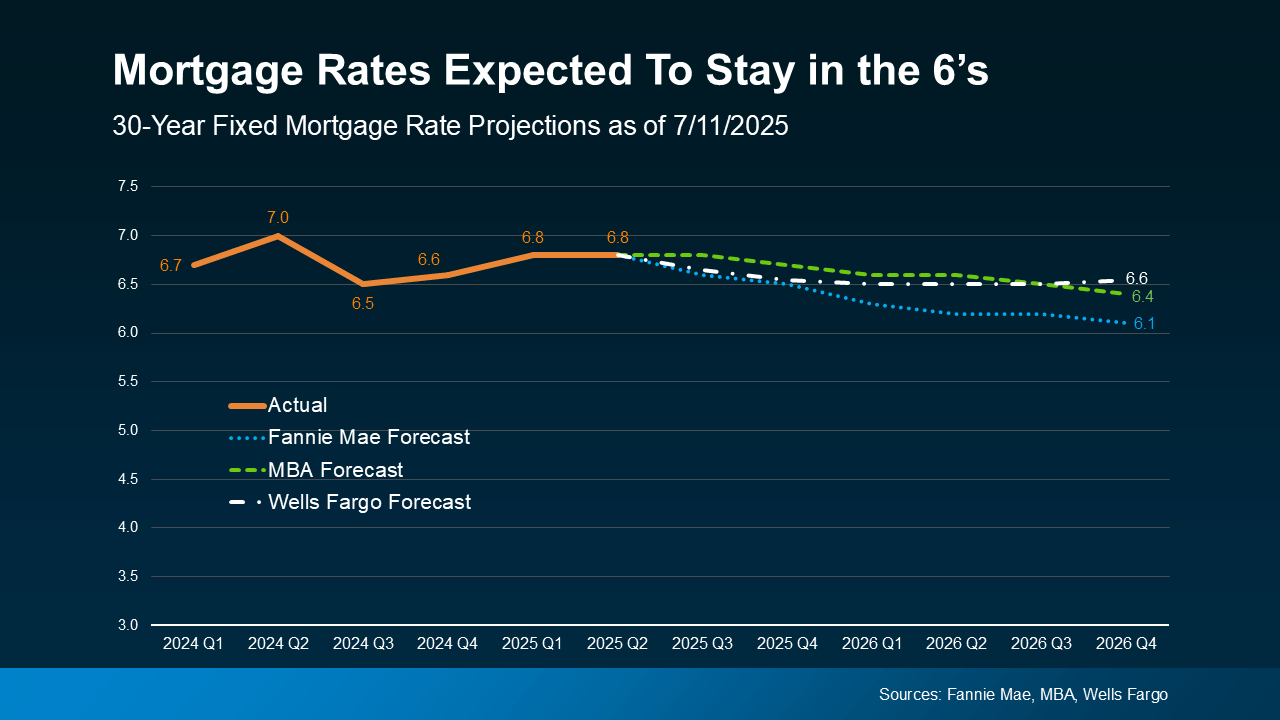

Mortgage Rates: As of July 18, the average 30-year fixed rate was 6.75%, up from 6.67% at the beginning of July. With rates expected to hold steady and inventory levels starting to improve, buyers who’ve been on the sidelines may find now is the time to act, despite ongoing affordability concerns.

-

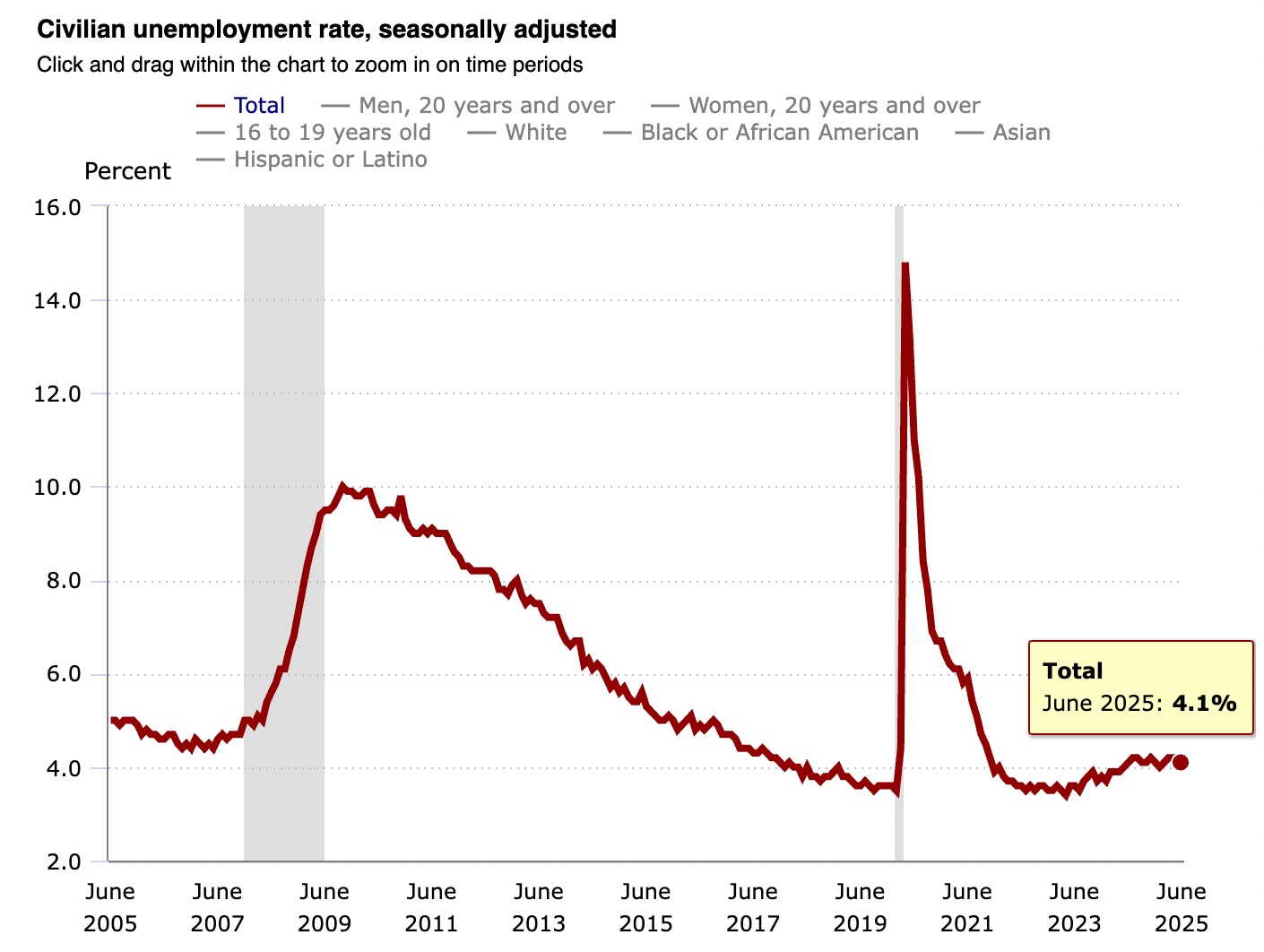

Job Cuts: Bay Area employers cut 6,800 jobs in June, marking the region’s second consecutive month of losses, according to the state Employment Development Department. All three major metro areas - San Francisco-San Mateo, the East Bay, and the South Bay - saw declines. In the first half of 2025 alone, the region shed over 24,000 jobs. Statewide, California now shares the highest unemployment rate in the nation with Nevada.

-

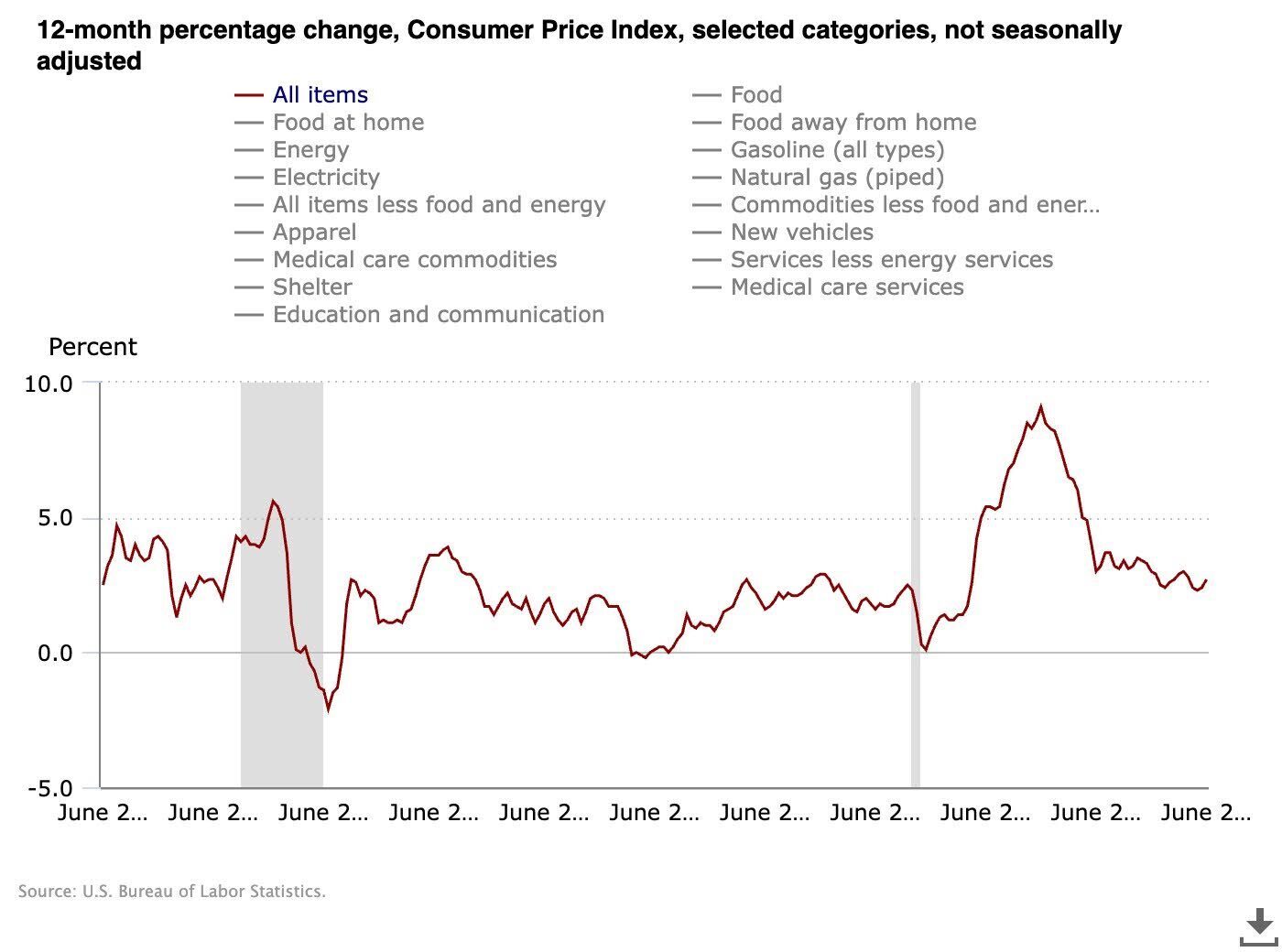

Inflation: Inflation is creeping back up, with June’s Consumer Price Index (CPI) showing a 2.7% annual increase, driven by rising shelter costs and new tariffs that are pushing prices even higher. For buyers, this means continued pressure on affordability as both home prices and everyday expenses remain elevated. For sellers, it signals a market where buyers are more price-sensitive, making accurate pricing and strong marketing essential. With the Fed holding interest rates steady to combat inflation, today’s market calls for smart, strategic decisions on both sides of the transaction.

-

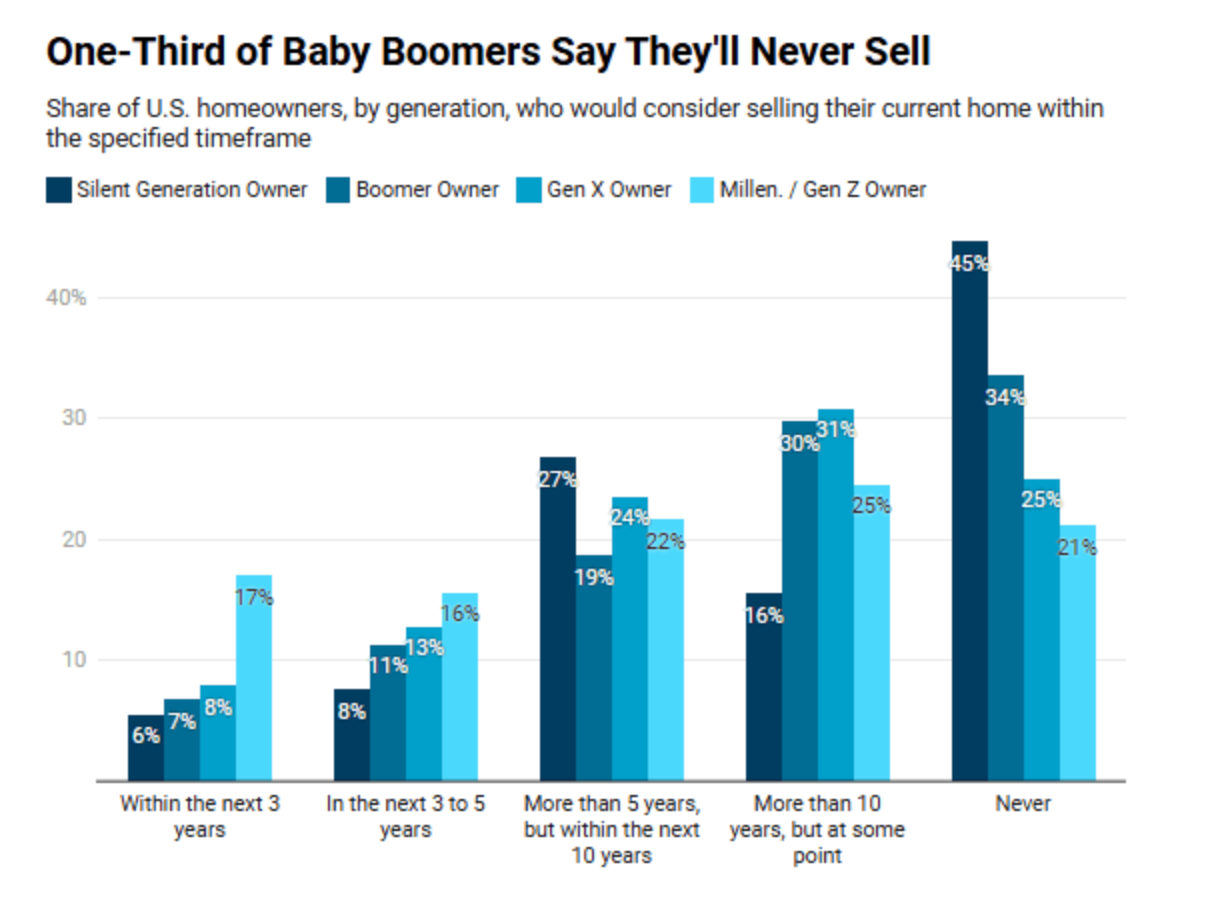

Homeowners Staying Put: According to a June Redfin survey, a third of Baby Boomers say they’ll never sell their home. The top reasons? Most simply love where they live (55%), many have paid off or nearly paid off their mortgage (20%), some think home prices are too high to buy again (16%), and a smaller group don’t want to give up their low mortgage rate (8%). We’ll see how this “Baby Boomer Effect” translates to listing inventory in the years to come.

-

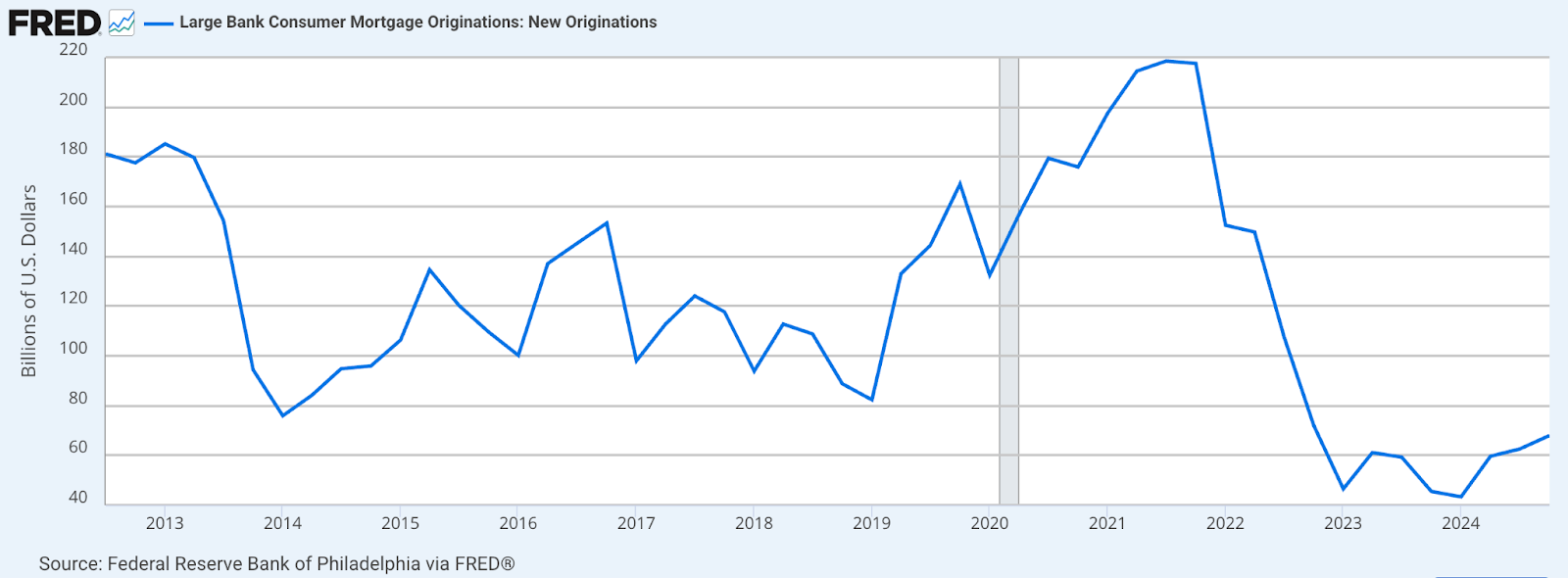

Loan Origination Volume is on the Rise: JPMorgan Chase and Wells Fargo posted strong mortgage origination gains in Q2 2025, outpacing seasonal forecasts. But tighter margins and ongoing rate volatility point to a still-fragile market beneath the volume boost.

-

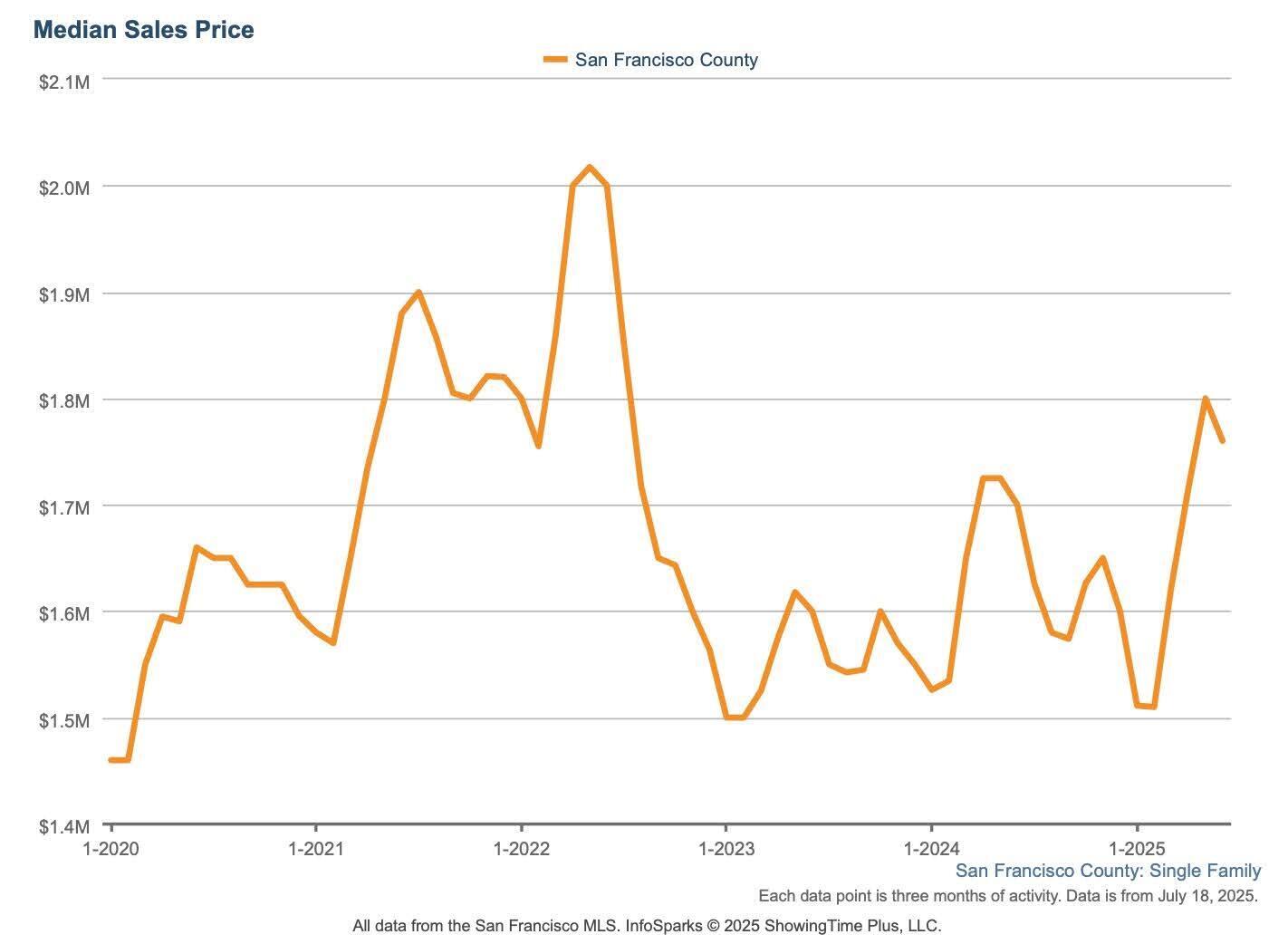

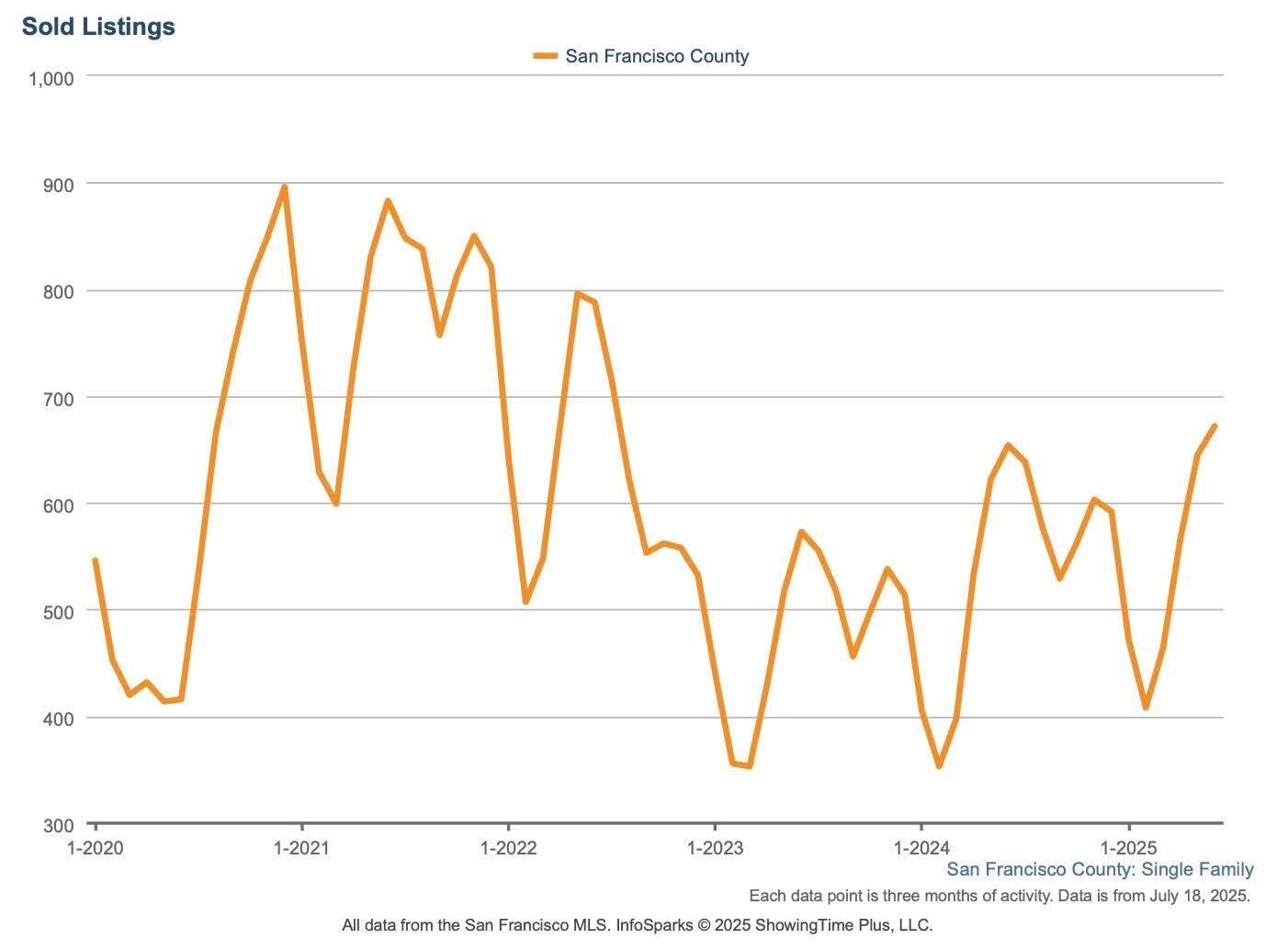

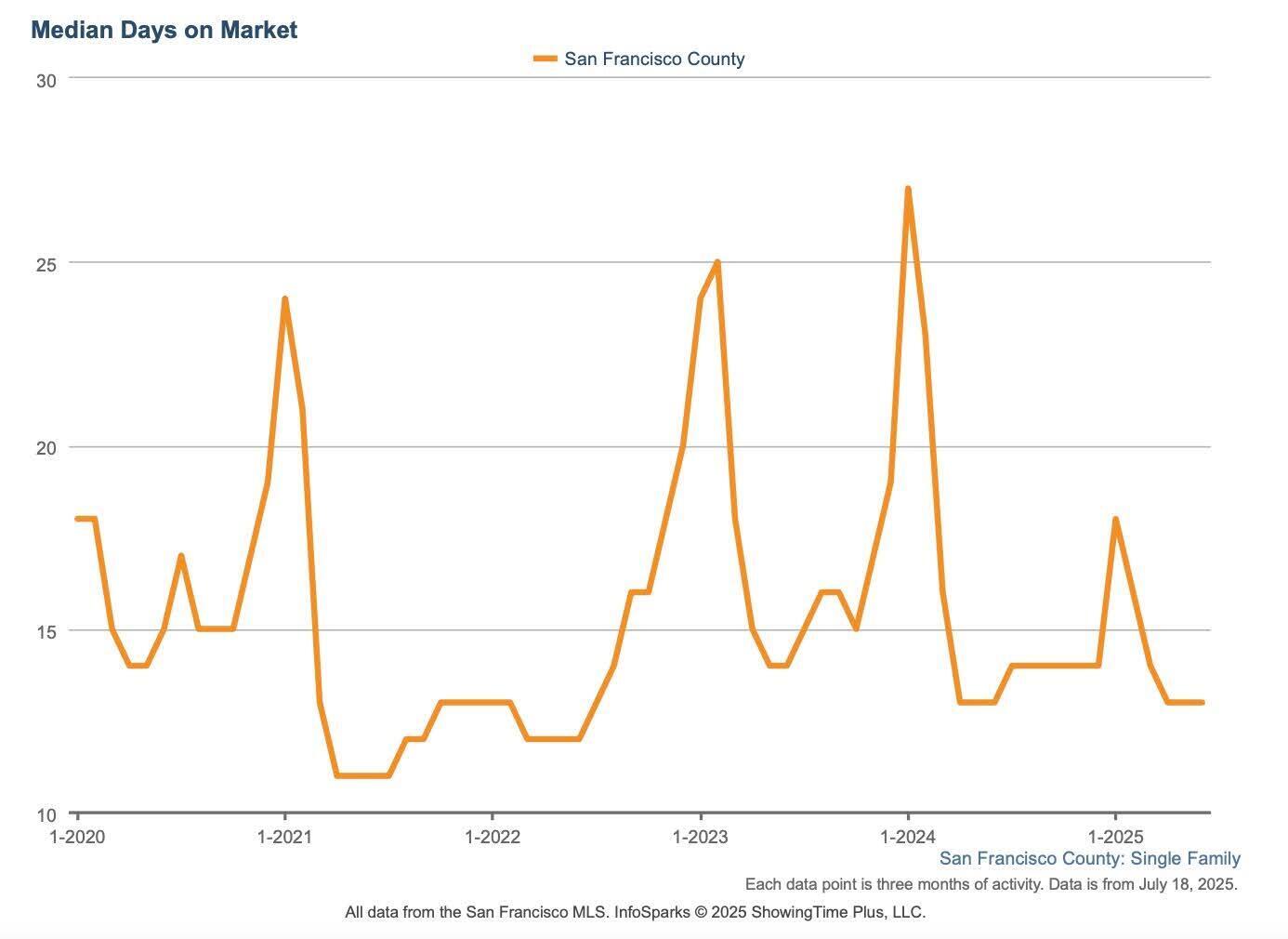

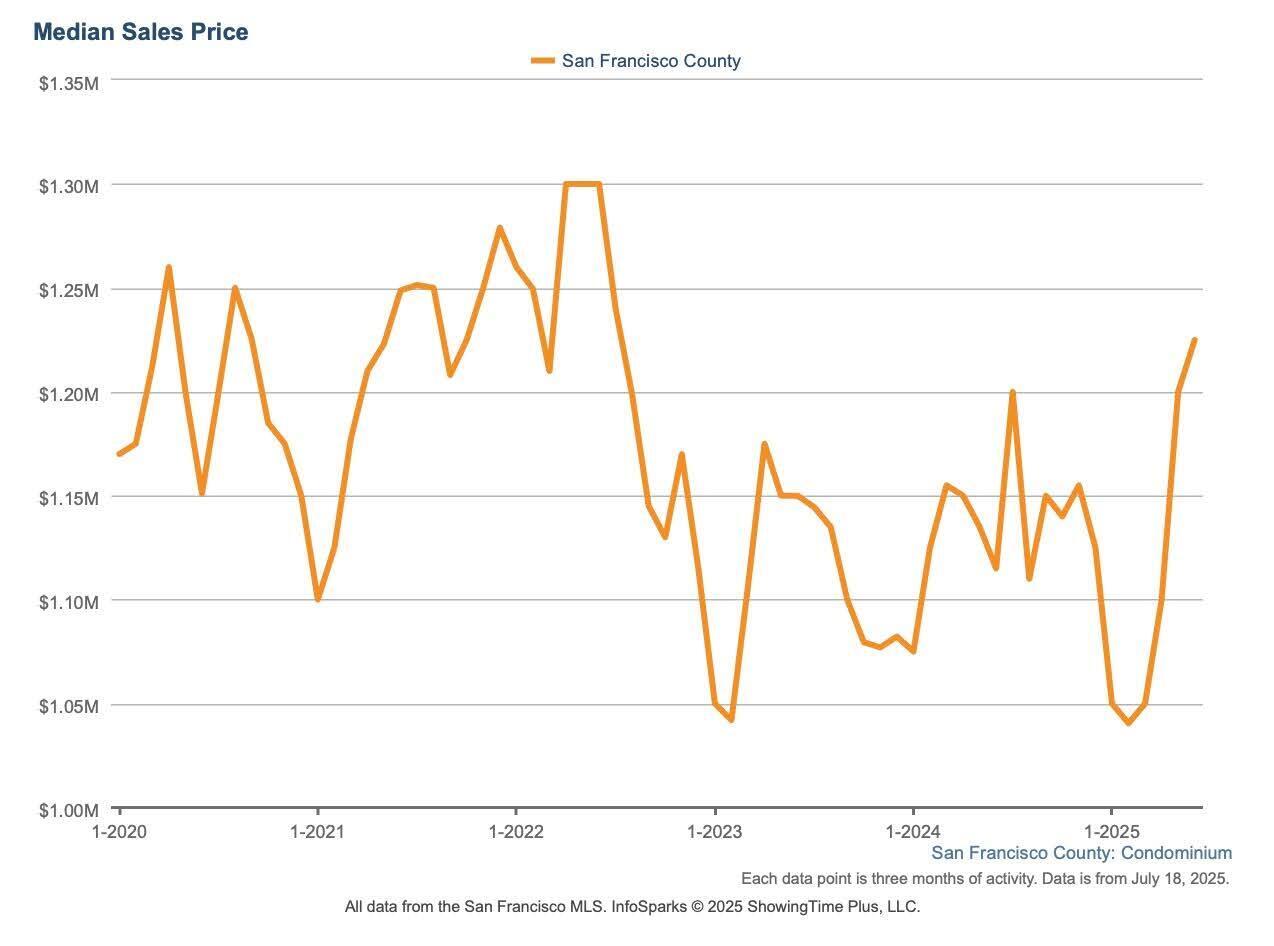

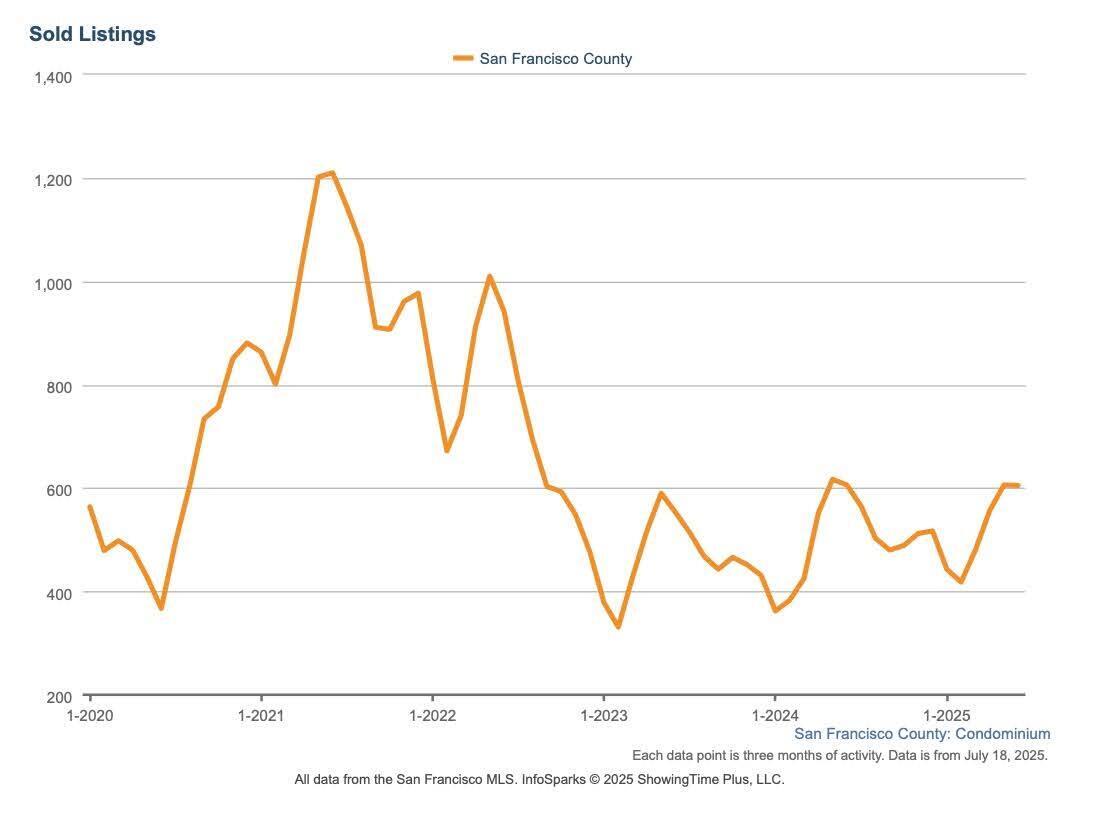

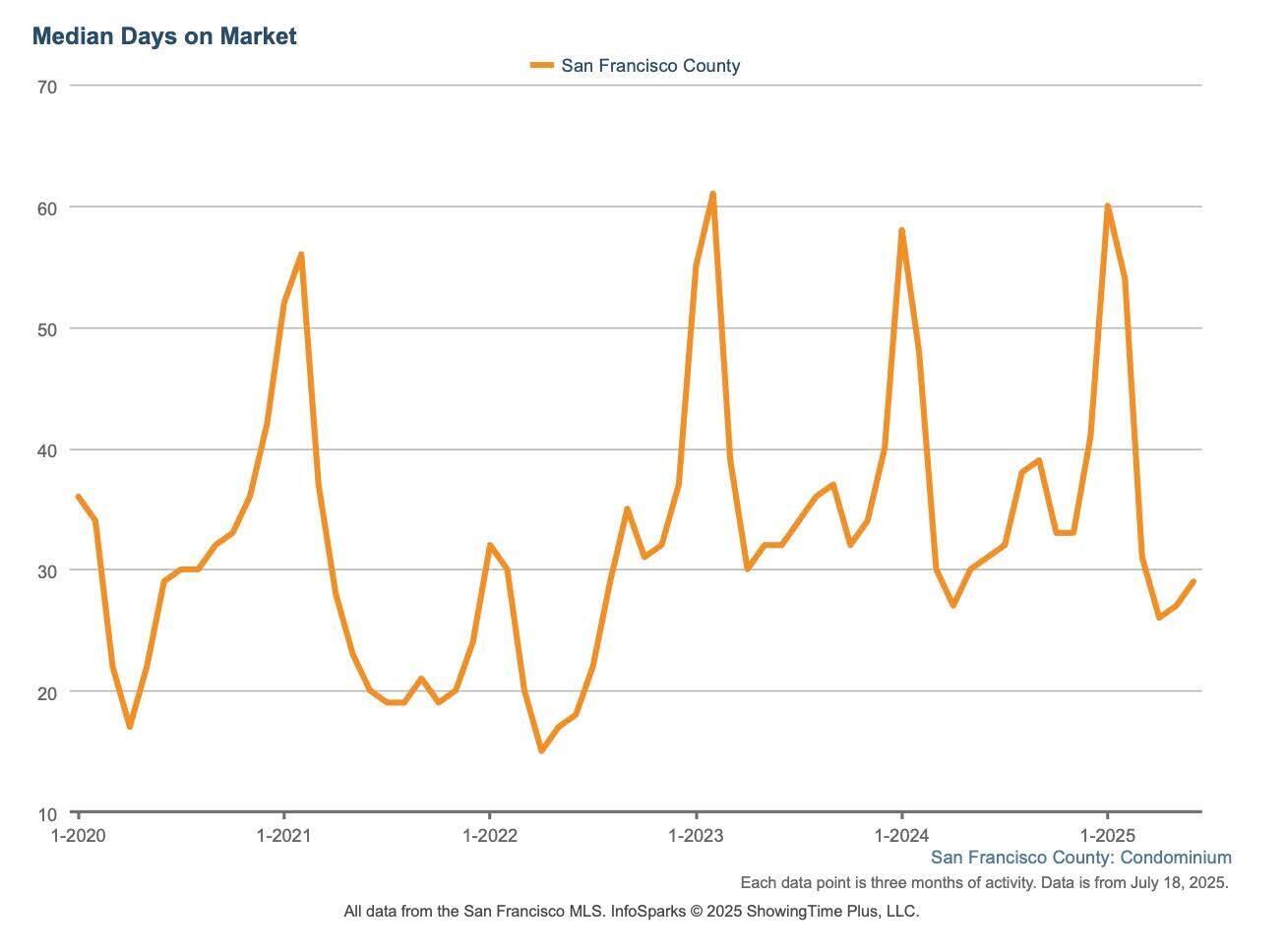

San Francisco Housing Prices: Single-family homes in San Francisco had a June 2025 median sales price of $1.76 million, down slightly from $1.8 million in May but up from $1.7 million in June 2024. Condos posted a median of $1.225 million, rising from $1.2 million in May and showing a strong 9.9% year-over-year increase. The overall median residential sales price, which includes all property types, was $1.465 million in June. This marks a slight dip from $1.5 million in May but a 2% increase compared to $1.437 million in June 2024. These figures reflect continued resilience in the San Francisco market, with buyer activity remaining steady despite elevated interest rates and broader economic challenges. See the charts below for a deeper breakdown by property type.

|

|

|