Spring fever is in full swing across San Francisco, and the market continues to defy expectations. Competition remains intense, inventory is still historically tight, and the influence of AI-driven wealth continues to fuel aggressive buyer demand, particularly among all-cash buyers competing against financed purchasers. Extraordinary bidding war stories are becoming commonplace: a Cow Hollow home recently closed at $15M after listing at $7.95M, while one of our recent Noe Valley listings sold for $3.5M after being offered at $1.995M.

What’s especially notable this year is that seasonality appears to be shifting. Rather than the typical summer slowdown, inventory is expected to continue flowing through the coming months as sellers attempt to capitalize on exceptionally strong pricing conditions.

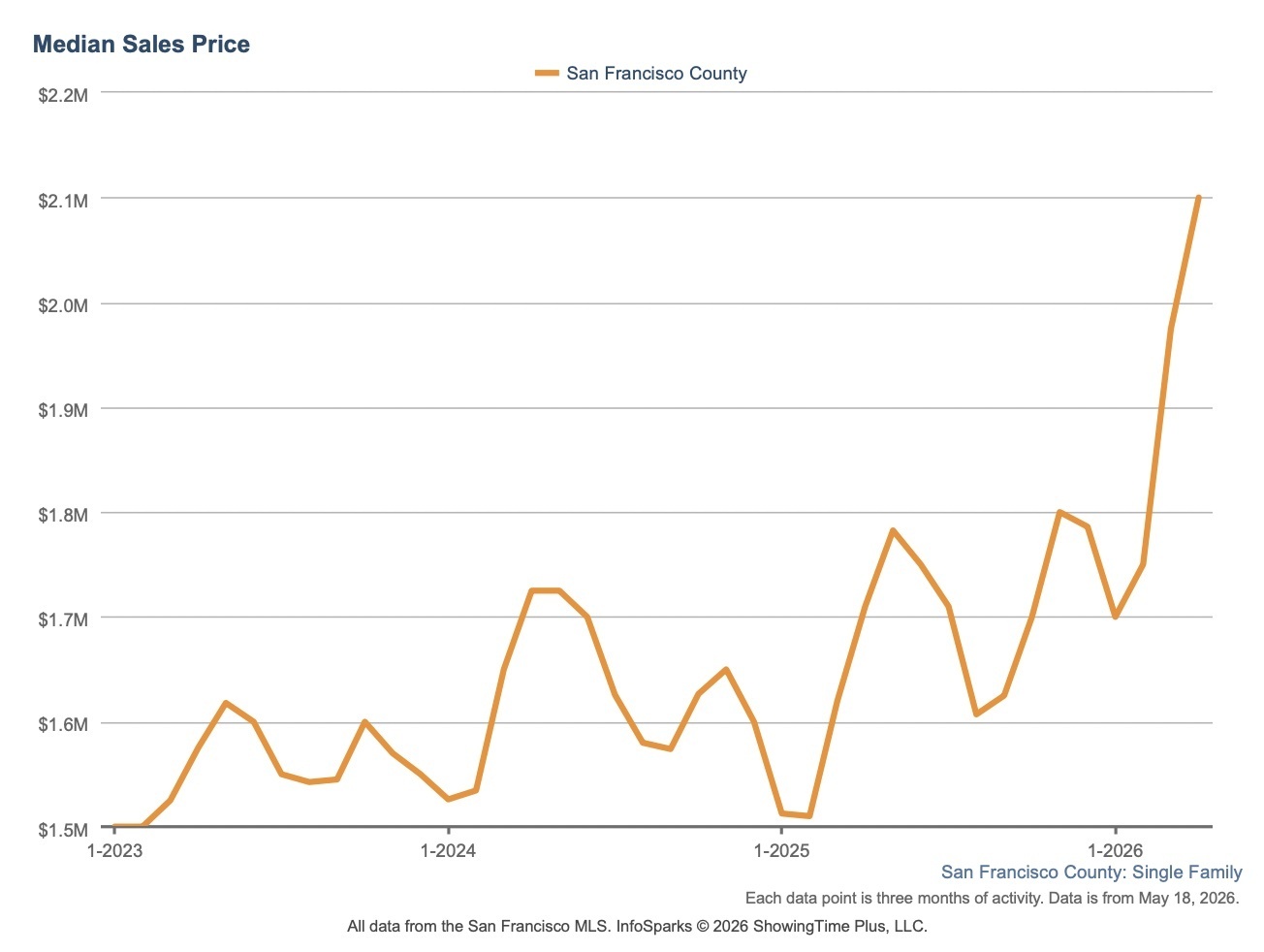

As of May 17, 800 single-family homes have sold in San Francisco this year, compared to 821 during the same period last year. While sales volume is relatively similar, pricing tells a dramatically different story.

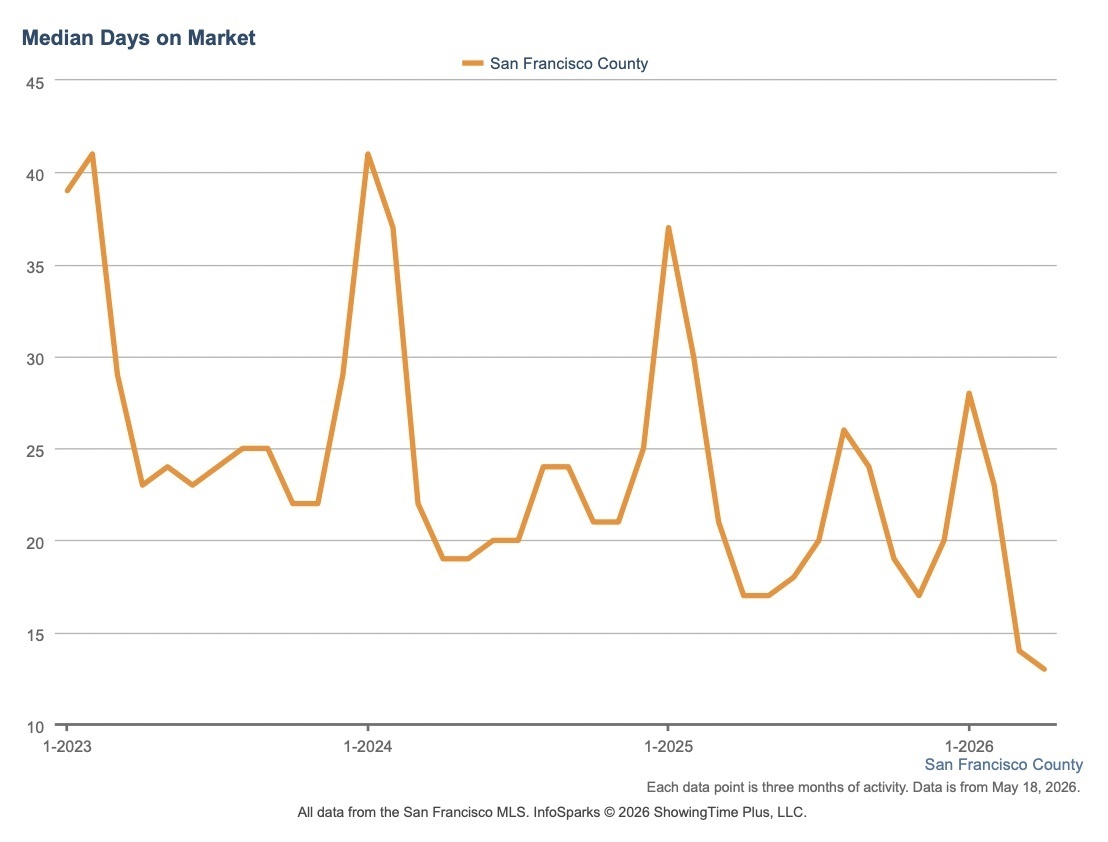

Of the 800 single-family homes sold year-to-date in 2026, the median list price was $1.652M, while the median closed price climbed to $2.091M - a staggering 26.65% above asking. Median price per square foot reached $1,163, while median days on market fell to just 11 days.

Compare that to the same period in 2025, when the median list price was $1.495M and the median closed price was $1.705M, representing 14.05% over asking. At that time, the median price per square foot was $1,045 and median days on market stood at 13.

In short: homes are selling faster, buyers are bidding far more aggressively, and pricing pressure has intensified substantially from just one year ago.

At the national level, however, the latest inflation data may cause some buyers to hesitate. April’s Consumer Price Index came in at 3.8%, reigniting concerns that mortgage rates could remain elevated longer than many had hoped. For financed buyers, even modest rate increases materially affect purchasing power, monthly payments, and borrowing capacity, creating a more cautious mindset nationally.

But San Francisco continues to operate differently from much of the broader U.S. housing market.

Here, historically low inventory, renewed optimism around the city’s economy, and continued inflows of AI-driven wealth are sustaining intense competition, particularly for well-located single-family homes. While higher inflation and mortgage rate volatility may sideline some financed buyers, all-cash and high-liquidity buyers remain extremely active, helping maintain upward pricing pressure despite broader economic uncertainty.

In many ways, the latest inflation data may actually reinforce urgency among buyers who fear rates could move even higher later this year. That “buy now before borrowing costs worsen” mentality continues to fuel aggressive bidding behavior across San Francisco’s most competitive neighborhoods.