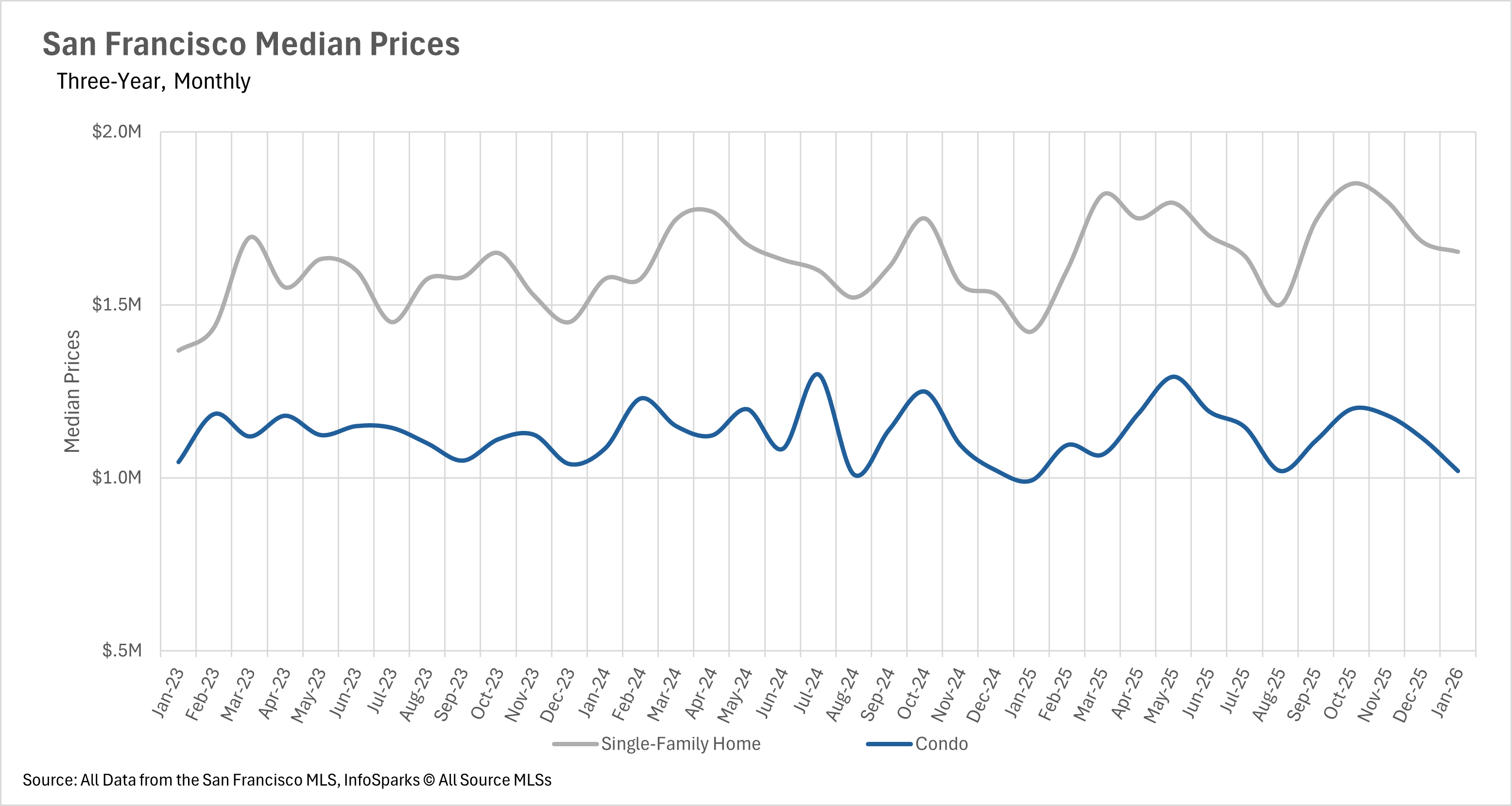

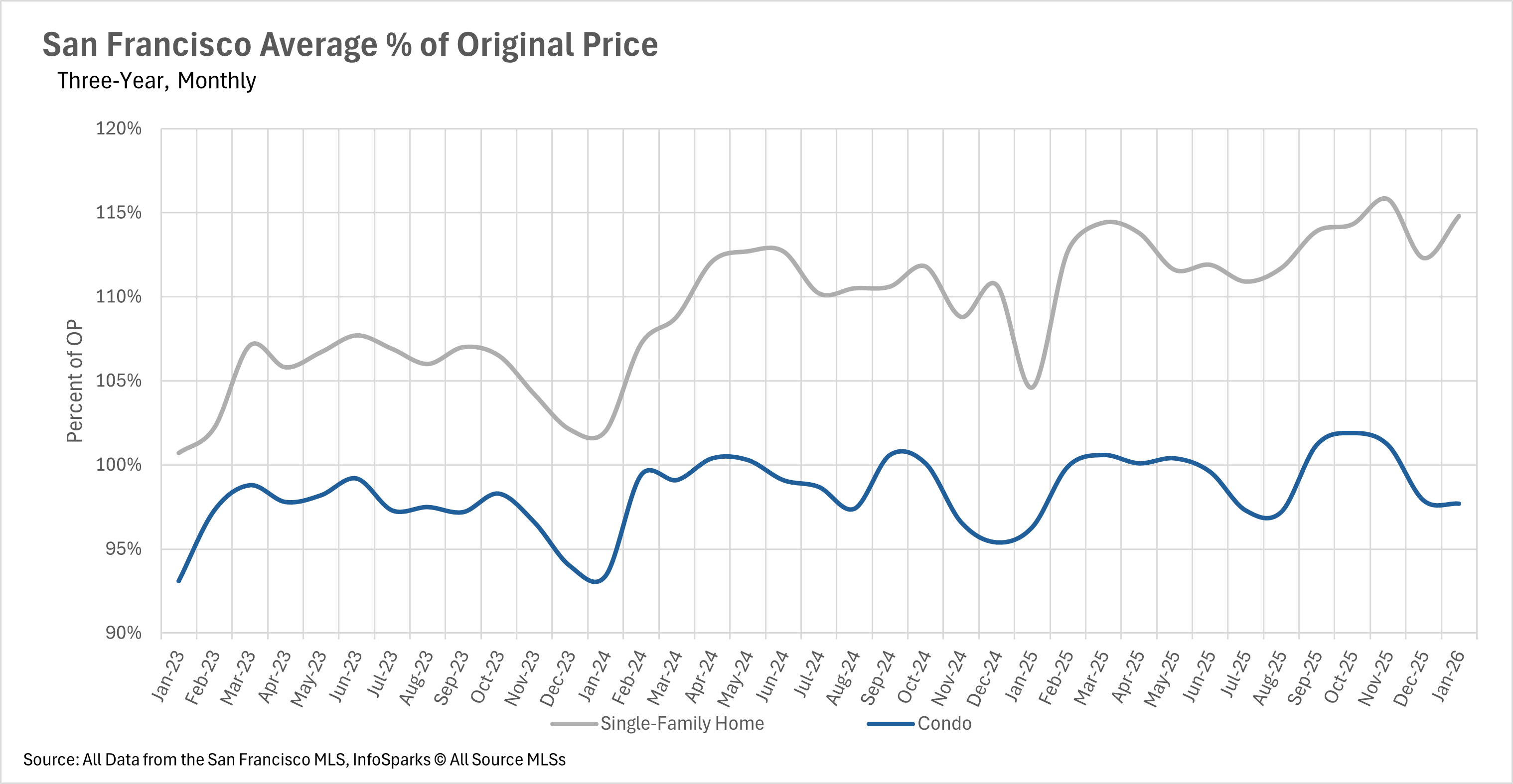

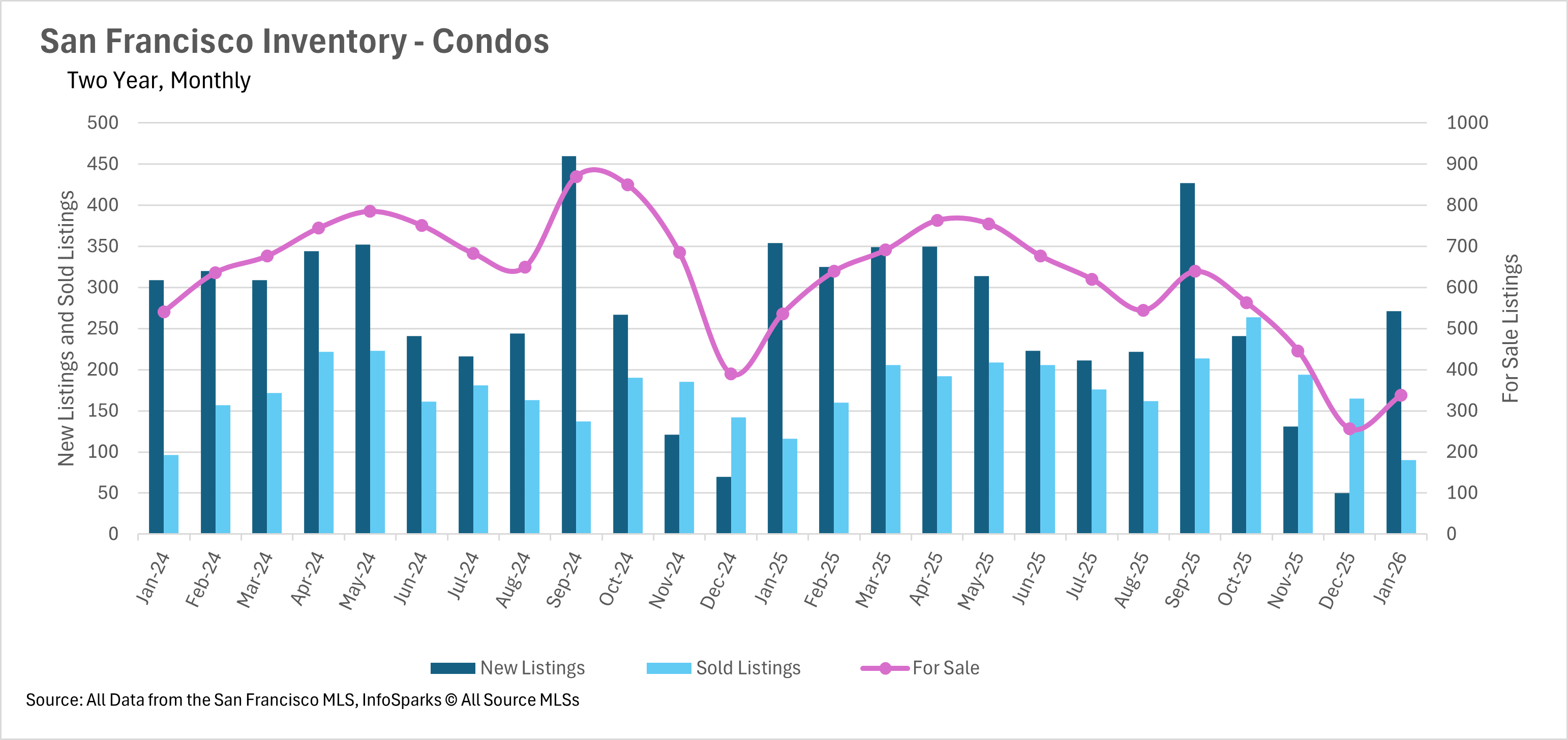

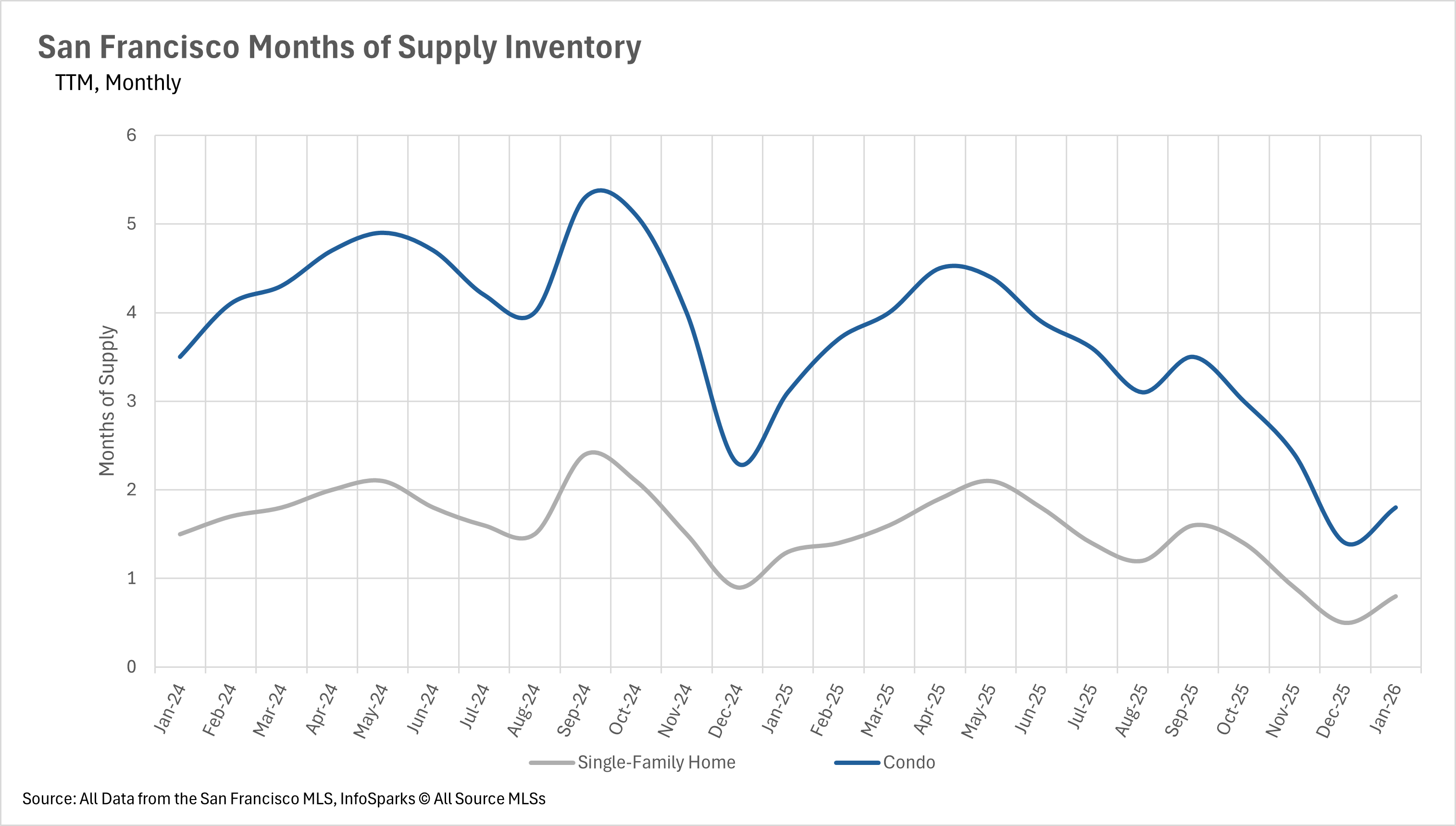

San Francisco’s bidding wars have carried straight into February, fueled by an extreme lack of inventory and very strong buyer demand. Brokerage sales meetings are once again filled with stories of multiple offers and highly competitive price outcomes.

Agents have been preparing their buyers accordingly. Those needing financing are being urged to move beyond simple pre-approval letters and complete full underwriting with trusted lenders, positioning them to compete more effectively with all-cash buyers, who are appearing with increasing frequency in competitive situations.

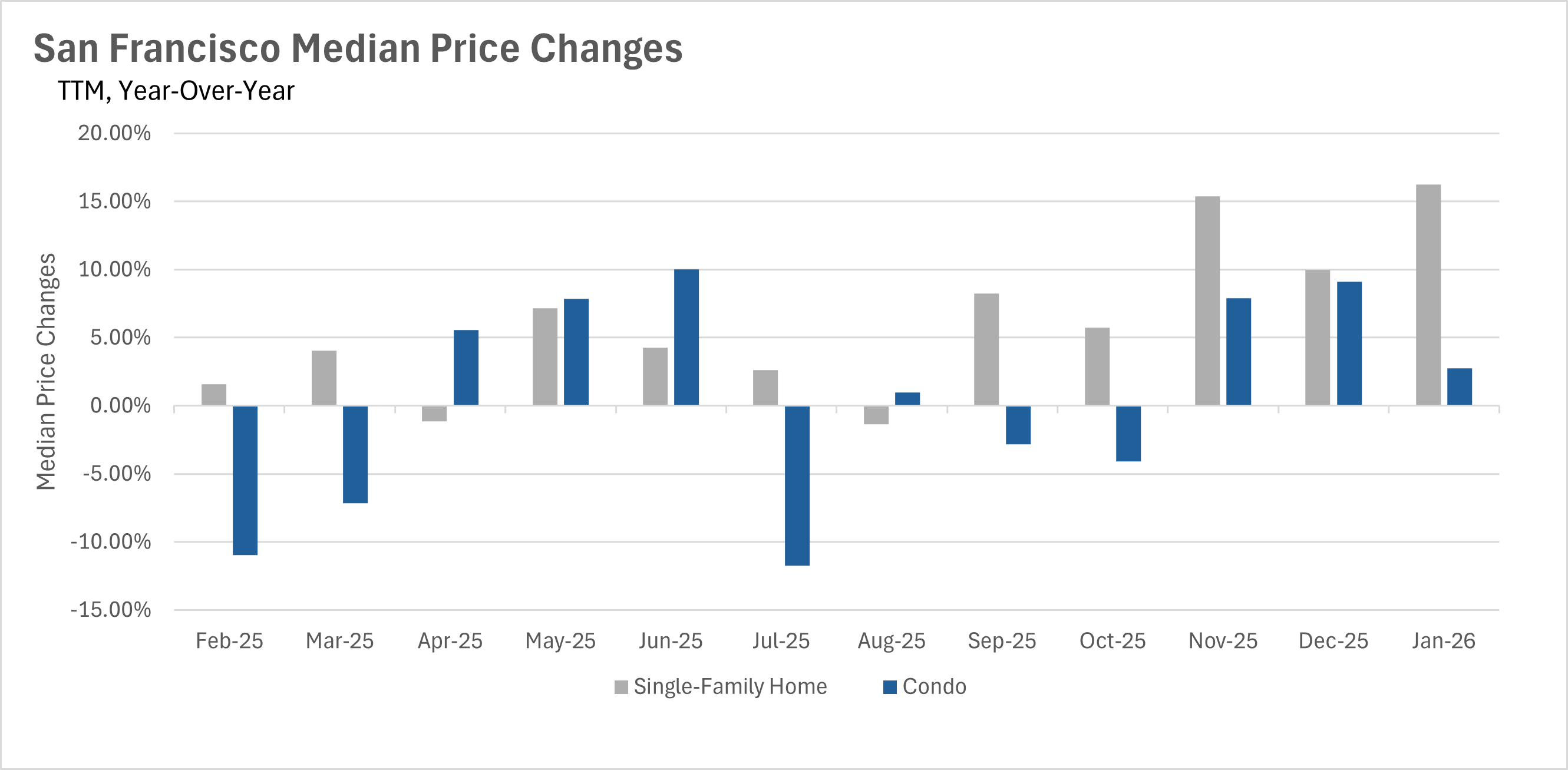

The data reinforces what we’re seeing on the ground:

27% of all single-family homes sold in San Francisco since January 1 were all-cash, up slightly from this time last year (26%).

The big change: for homes sold over $3M, that figure rises to 53%.

At this time last year, just 29% of $3M+ sales were all cash.

The continued influx of AI-driven capital, combined with renewed global attention on San Francisco and sustained renter demand, has created a powerful demand backdrop. With supply still constrained, competition remains intense, particularly for well-located, thoughtfully prepared homes.

As always, markets evolve. But for now, the imbalance between supply and demand is clear, and sellers who enter the market strategically are finding meaningful leverage.

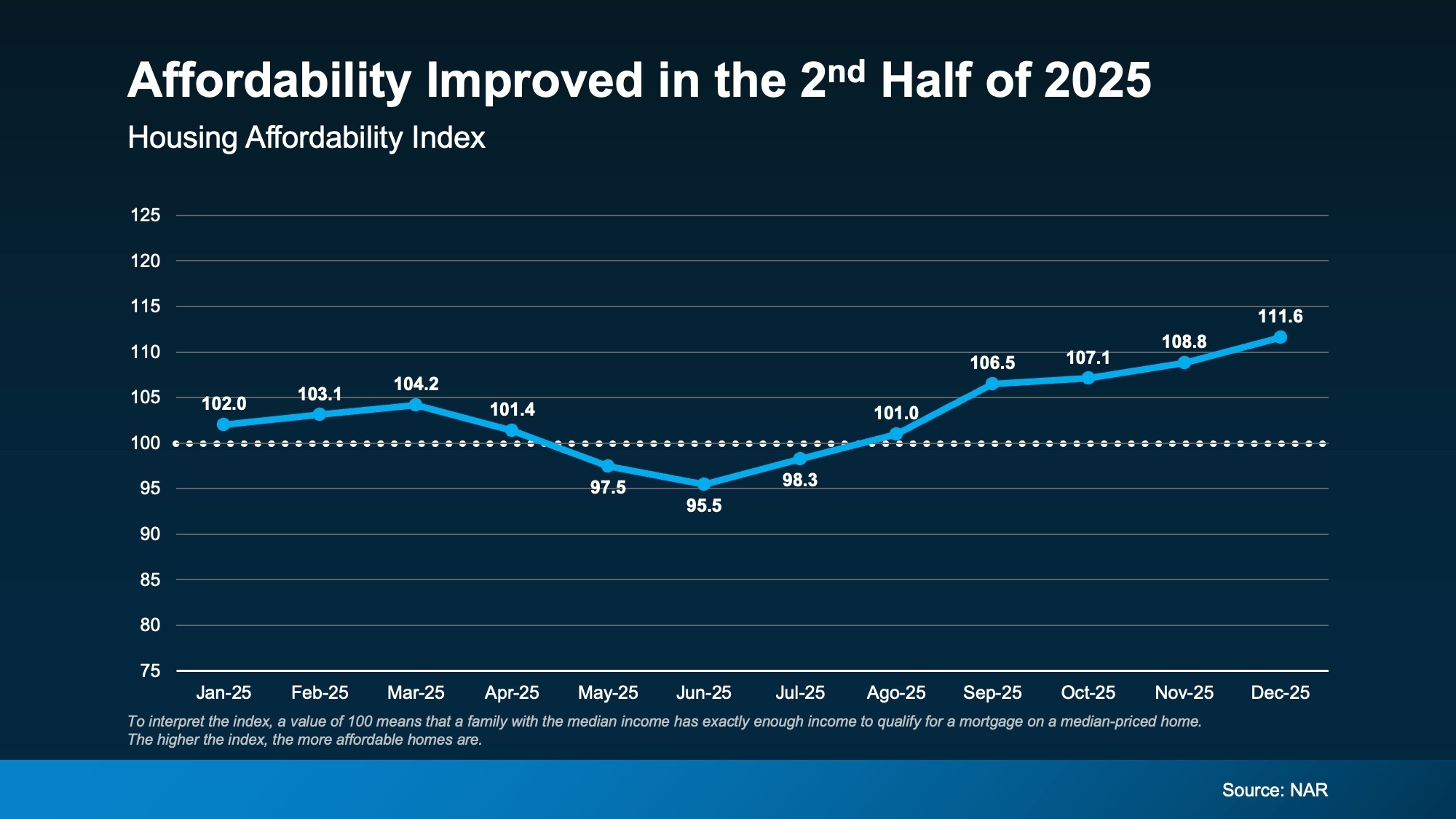

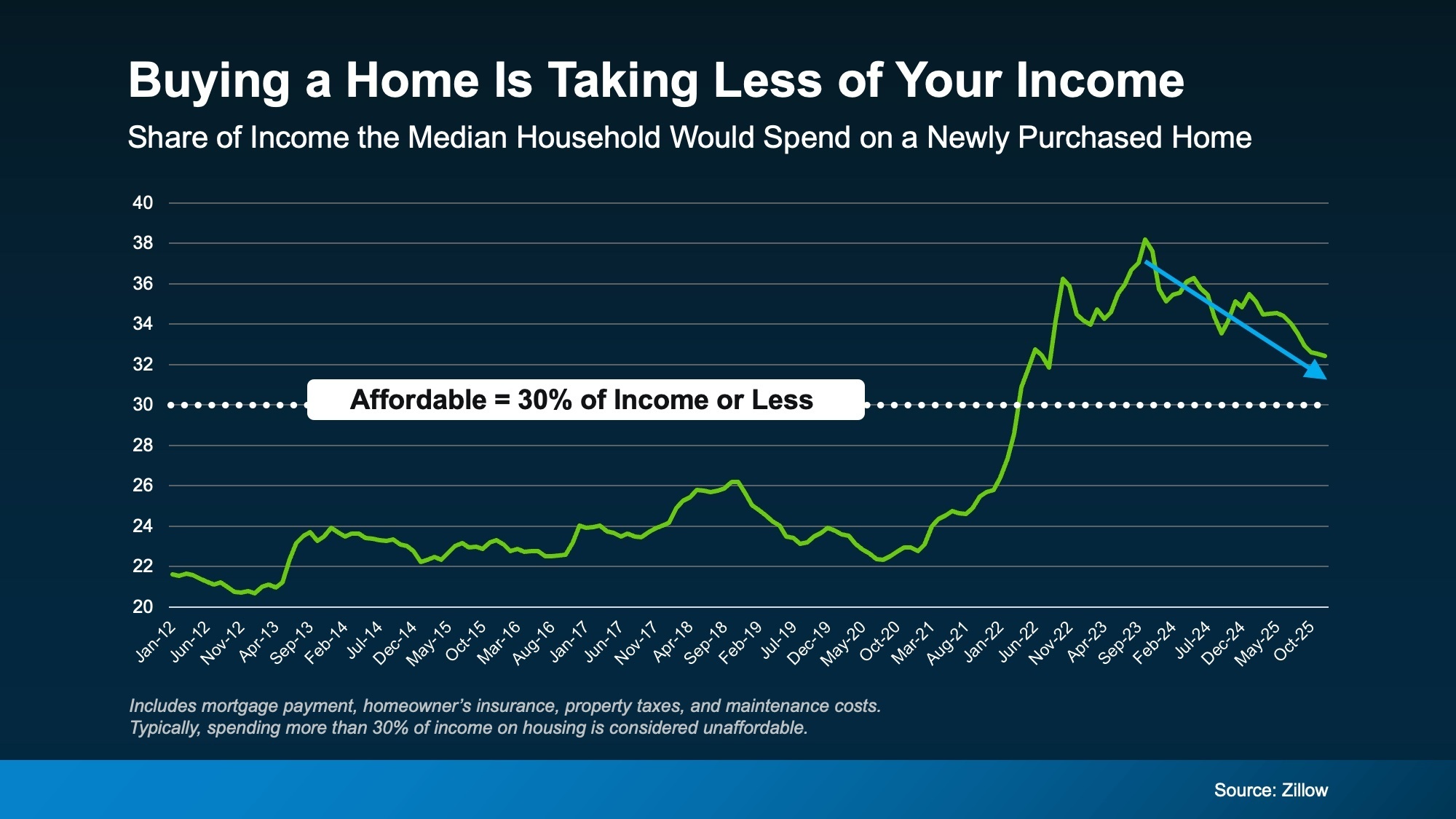

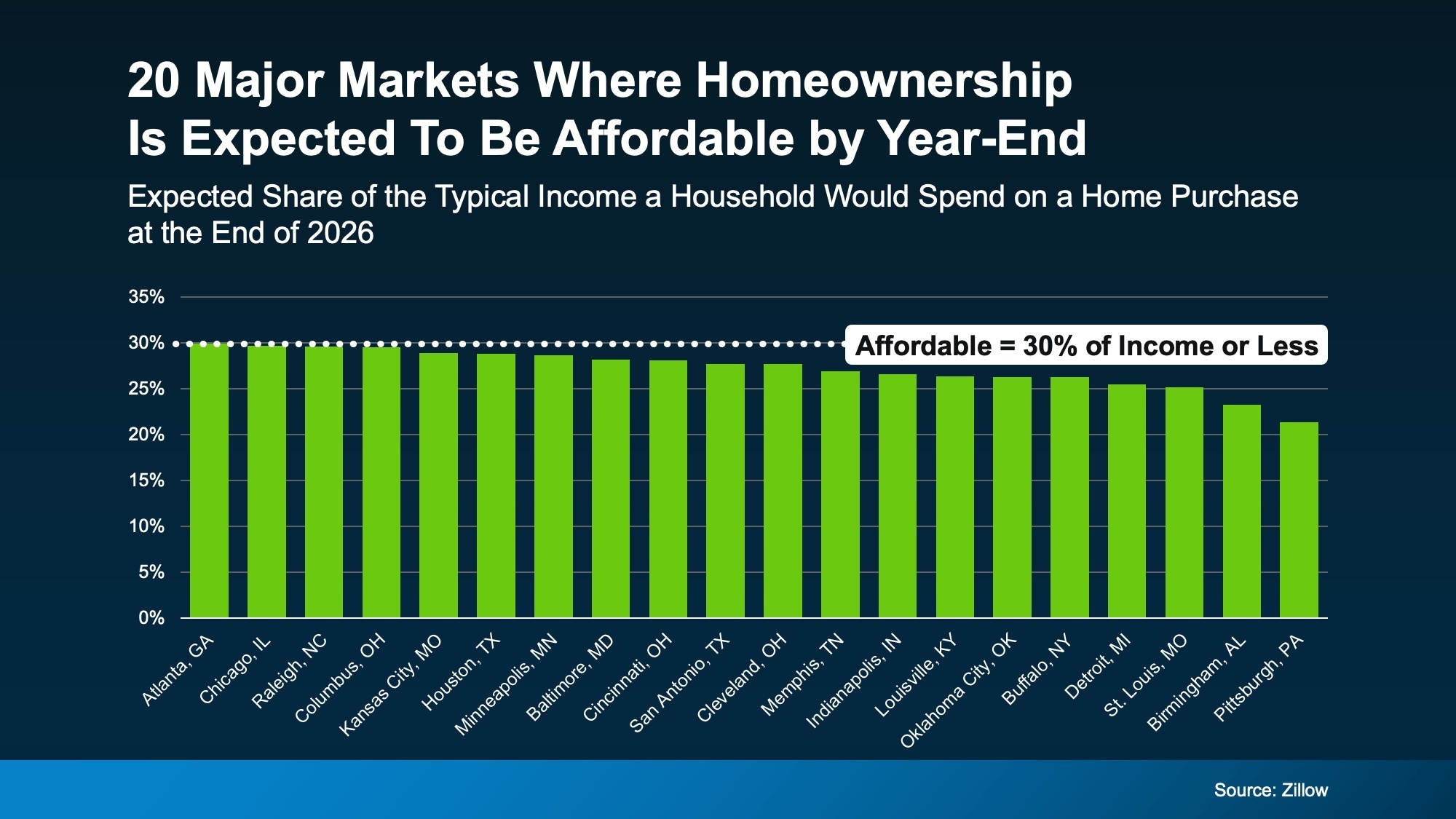

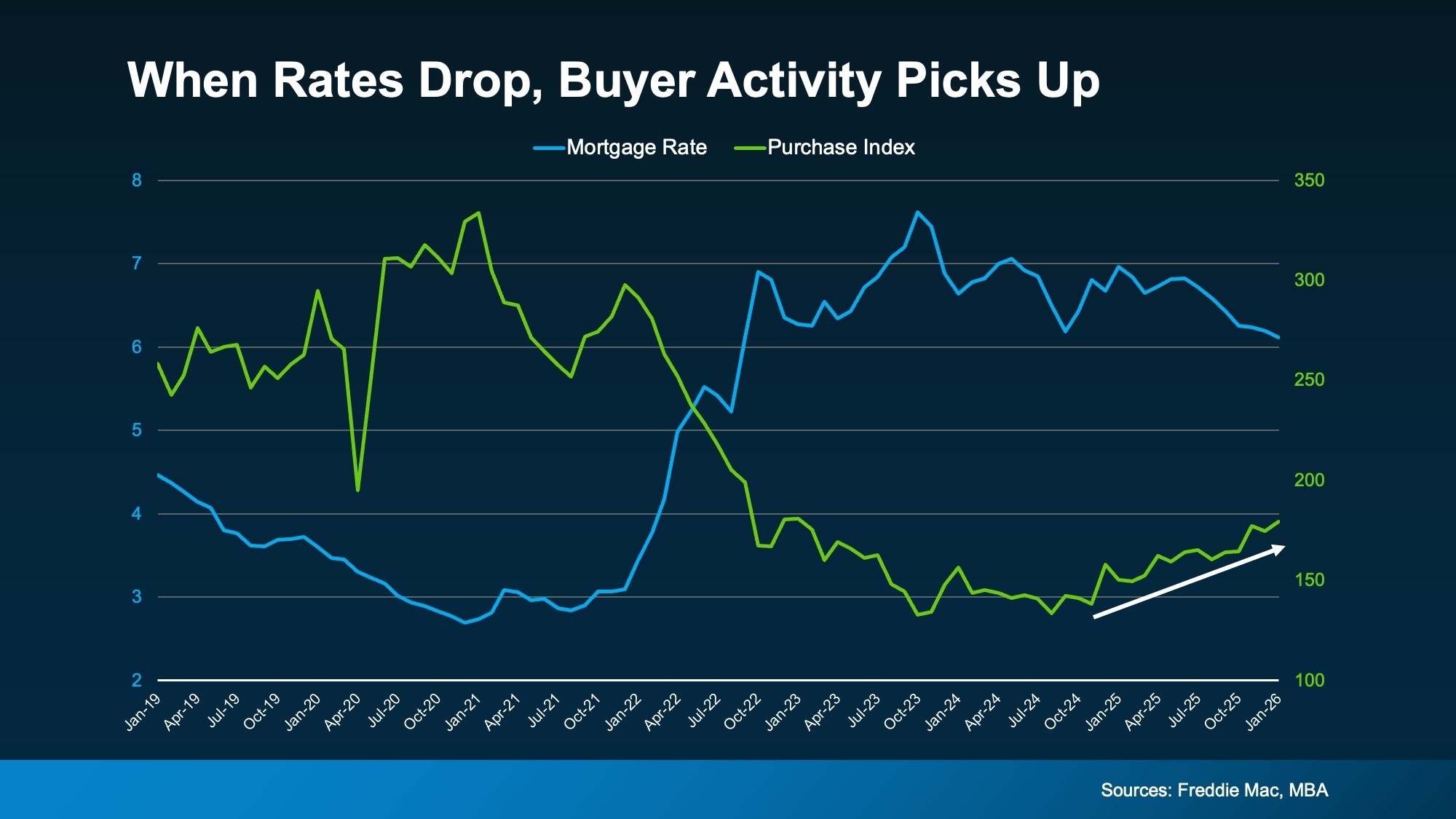

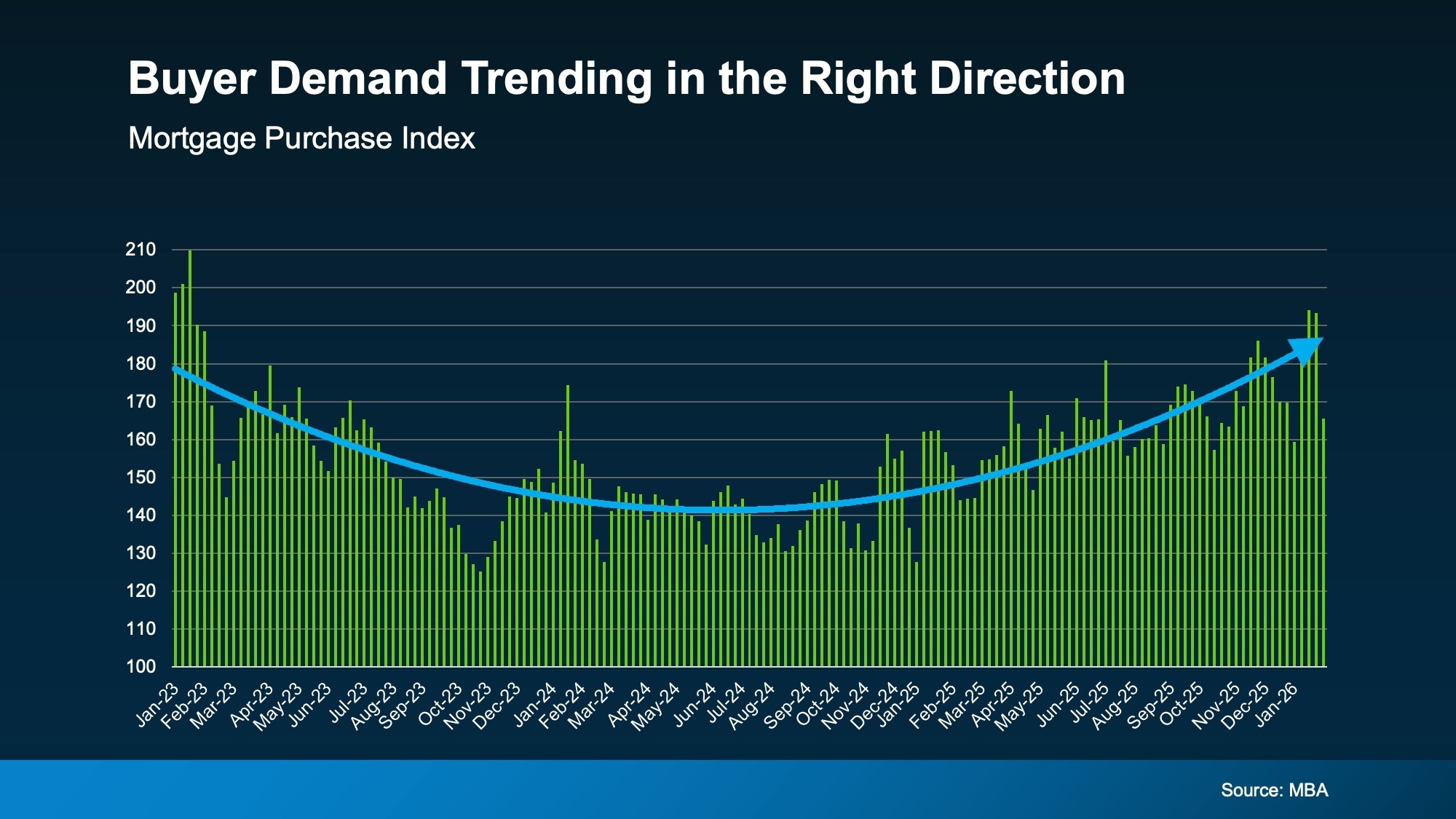

Nationally, the trend has begun to shift. After several years defined by one of the most challenging affordability environments in modern housing history, conditions improved in the second half of 2025. Home prices have largely stalled, rates have eased from their peak, and affordability has modestly recovered. According to Zillow, the typical mortgage payment now consumes 32.5% of median household income - the most favorable reading since August 2022.

That marks a meaningful change from the sharp reset we experienced when mortgage rates jumped from roughly 3% in 2021 to above 7% in 2023, pushing the typical monthly payment more than $1,000 higher than pre-pandemic levels. That surge sidelined many would-be movers and slowed the market’s pace. Today, while affordability is not yet back to historic norms, the direction of travel is notably more constructive.